Microbrewer Wins Property Tax Challenge

Craft breweries have exploded in Michigan in recent years, with the number operating in Michigan dramatically increasing from 105 in 2011 to 398 in 2020, the 6th highest in the country.

Michigan brewers should be aware of how their growing businesses are impacted by state and local tax, including personal property tax, as demonstrated by a recent Tax Tribunal decision.

A Michigan-based microbrewer qualified for a personal property tax exemption, according to a Michigan Tax Tribunal decision issued September 2, 2021. The microbrewer, Dragonmead, LC, brews beer and other alcoholic beverages at its brewery in Warren, Michigan. The beverages brewed are sold at retail at the Warren brewery, at retail through the microbrewer’s restaurant in St. Clair Shores, and at wholesale to several distributors. The City of Warren denied the microbrewer’s personal property tax exemption claim, taking the position the production of beer sold other than through the microbrewer’s retail locations meant the property did not qualify as exempt. The Tax Tribunal disagreed with the city, finding the microbrewer’s personal property was exempt under the eligible manufacturing personal property exemption.

The microbrewer’s operations

The microbrewer claimed its personal property located at the brewery in Warren was exempt under the eligible manufacturing personal property tax exemption. Over 50% of the property was used for brewing alcoholic beverages, specifically craft beer. The two brewing systems used on site moved and converted raw materials through the production process, starting with cracking malt through a grain mill to fermentation and bottling, packaging, and storage. In 2019, of the total production, 24% was sold at the brewery in Warren, 3% was sold at the microbrewer’s restaurant in St. Clair Shores, and 73% was sold to wholesale distributors. In 2020, 21% was sold in Warren, 14% was sold in St. Clair Shores, and 65% was sold at wholesale.

The property tax exemption explained

All real or personal property in Michigan is generally subject to property tax, unless specifically exempt. MCL 211.1. In 2012, to support Michigan manufacturers as well as encourage new business in the state, the Michigan Legislature passed laws treating qualifying personal property related to manufacturing operations as exempt from property tax. The exemption is called the eligible manufacturing personal property (“EMPP”) tax exemption. There are a number of steps used to determine whether property qualifies as EMPP, as set forth in MCL 211.9m and MCL 211.9n of the General Property Tax Act:

- Occupied real property. Determine what real property the taxpayer’s operations occupy in one city or township, called the “occupied real property.” This may be one parcel, contiguous parcels, or part of a parcel, depending on the ownership and occupancy of the real property parcels involved.

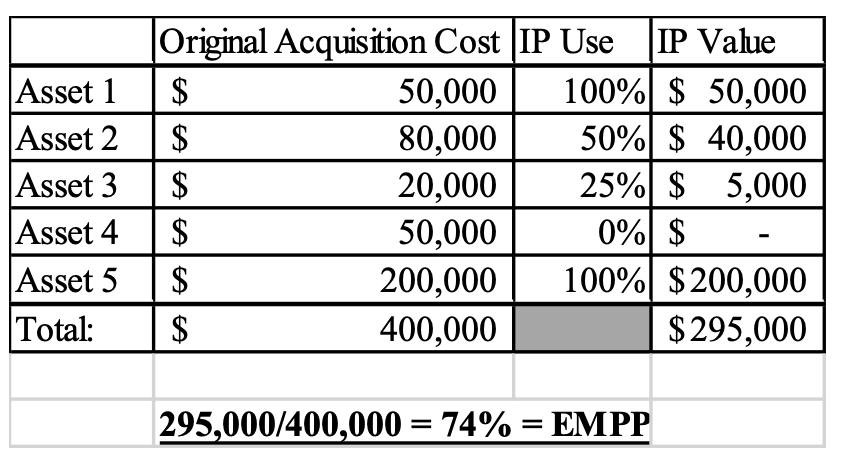

- Industrial processing use. Next, determine what percentage of each personal property asset located on the occupied real property is used for industrial processing or direct integrated support and whether it is used 100%, 0%, or something in between. Multiply each asset’s industrial processing percentage by the asset’s original acquisition cost to get the value of each asset’s industrial processing use.

Industrial processing defined. Property used in industrial processing has been exempt from sales and use tax in Michigan since 1939. Industrial processing is a complicated term, often modified and expanded by the Michigan Legislature over the years, and often disputed between taxpayers and the State of Michigan. In determining whether personal property is exempt from property tax under the EMPP exemption, the EMPP statutes lean on the definition of industrial processing from the Michigan sales and use tax acts.

"Industrial processing" means “the activity of converting or conditioning tangible personal property by changing the form, composition, quality, combination, or character of the property for ultimate sale at retail or for use in the manufacturing of a product to be ultimately sold at retail. Industrial processing begins when tangible personal property begins movement from raw materials storage to begin industrial processing and ends when finished goods first come to rest in finished goods inventory storage.” MCL 205.54t; MCL 205.94o.

Direct integrated support defined. Unlike “industrial processing, “direct integrated support” is not a historical concept borrowed from the Michigan sales and use tax acts. It is, instead, a new term adopted for the EMPP exemption which broadens the concept of industrial processing to include activities that “support” an industrial process, including research and development; testing and quality control functions; engineering; receiving or storing equipment, materials, supplies, parts, or components for industrial processing, or scrap materials and waste resulting from industrial processing; storing of finished goods inventory; and sorting, distributing, or sequencing functions related to transportation and just-in-time inventory. The key to being used for direct integrated support is that the asset is related to and/or supporting the industrial process.

- Eligible manufacturing personal property determination – all or nothing. Add together all the values of the assets’ industrial processing use, by original acquisition cost calculated above in (2). Then divide this sum by the total original acquisition cost of all the personal property on the occupied real property. If the result is over 50%, all the personal property on the occupied real property is deemed to be used predominately in industrial processing or direct integrated support; and all the personal property is “eligible manufacturing personal property” or EMPP. If the result is less than 51%, then none of the personal property on the occupied real property is eligible for the exemption.

- Claiming the exemption. If the personal property on the occupied real property qualifies as EMPP, then those assets defined as “qualified new personal property,” placed in service (or construction in progress) after December 31, 2012, and “qualified previously existing personal property,” placed in service more than 10 years before the current calendar year, are exempt. The exemption is claimed each year by timely filing Michigan Department of Treasury Form 5278.

Microbrewer’s assets are EMPP

In 2020, the microbrewer claimed its assets used at the brewery in Warren qualified for the EMPP exemption. The City of Warren denied the microbrewer’s exemption claim, and the microbrewer appealed the denial to the Michigan Tax Tribunal. The parties agreed the property at issue was more than 50% of the value of all of the personal property on the occupied real property. And the parties agreed the property at issue was used to brew alcoholic beverages (“the brewing assets”). The dispute centered on whether the brewing assets were used for industrial processing. If so, then all the personal property at the brewery in Warren qualified as EMPP.

The City of Warren contended the brewing assets were not used for industrial processing to the extent they were used to produce alcoholic beverages for retail sale at locations other than those owned by the microbrewer. In other words, the wholesale sales to distributors disqualified the assets as being used in industrial processing.

The Tax Tribunal concluded the assets were used to convert malt, water, hops, and yeast into beer, which were clearly industrial processing activities. The City of Warren contended two subsections within the industrial processing definition in MCL 205.94o, however, changed this conclusion:

- “Tangible personal property used for the preparation of food or beverages by a retailer for ultimate sale at retail through its own locations, except as provided in subsection (4)(h)” is not eligible for the industrial processing exemption. MCL 205.94o(5)(h).

- “Tangible personal property used or consumed in an industrial processing activity to produce alcoholic beverages that are sold at retail by that industrial processor through its own retail locations” is eligible for the industrial processing exemption. MCL 205.94o(4)(h).

Making various statutory interpretation arguments, the City of Warren concluded assets used to produce alcoholic beverages for wholesale sales were not used for industrial processing. The Tax Tribunal disagreed. The Tribunal determined the statutes reviewed were not ambiguous, did not conflict, and therefore should be interpreted based on their plain meaning. The Tribunal held that the microbrewer’s assets used to convert malt, water, hops, and yeast were used in an industrial process as the term was defined (citation above). Subsections (5)(h) and (4)(h) state only that producing food and beverages – except alcoholic beverages – for sale at retail at the producer’s own locations is not exempt industrial processing. Under the general definition of industrial processing, equipment used to produce alcoholic beverages, whether for retail sales or wholesale sales, are exempt; and subsection (5)(h) and (4)(h) do not change this outcome.

The Tax Tribunal’s holding is consistent with Elias Brothers Restaurants, Inc v Treasury Department, 452 Mich 144 (1996). In Elias Bros, the Michigan Supreme Court determined equipment used to produce food for Big Boy restaurants was used in industrial processing. The food was prepared at a 250,000 square-foot food processing and distribution facility located (ironically) in Warren, Michigan. The production center was physically separate from the Big Boy restaurants and treated as a distinct business operation, separate from the restaurants. As of 1996, the industrial processing exemption provision, MCL 205.94, stated “the preparation of food and beverages by a retailer for retail sale” was not industrial processing.

Over time, the industrial processing exemption language has changed. However, the result is still the same: producing food and beverages for wholesale is an industrial process, but producing them for retail sale at the producer’s retail location is not, except the production of alcoholic beverages for sale at the producer’s own retail locations.

Cheers to the microbrewery on its legal victory!

This type of tax dispute, however, is not limited to brewers. Any taxpayer engaged in some form of industrial process, product development, or manufacturing, may face similar disputes with taxing authorities. Novara Law represents taxpayers in property tax involving the EMPP exemption, as well as in sales and use tax disputes regarding the industrial processing exemption.

Side"bar"

-

A microbrewer is defined in the Michigan Liquor Control Code as “a brewer that manufactures in total less than 60,000 barrels of beer per year and that may sell the beer manufactured to consumers at the licensed brewery premises for consumption on or off the licensed brewery premises and to retailers …” MCL 436.1109(5).

- Craft breweries have exploded in Michigan in recent years. See https://www.brewersassociation.org/statistics-and-data/state-craft-beer-stats/?state=MI, accessed September 28, 2021.

- Challenges to taxes on alcoholic beverages have been a part of the history of the United States since the Constitution was ratified. The 1791 Whiskey Tax – the first federal excise tax – was wildly unpopular with farmers, as grain was the chief ingredient of whiskey. The “Whiskey Rebellion” ensued as a protest against the federal tax levied on both domestic and imported alcohol. After farmers attacked federal tax collectors in protest, “President George Washington dispatched a force of nearly 13,000 militia to put down a feared revolt. Resistance, however, dissipated when the troops arrived.” See https://history.house.gov/Historical-Highlights/1700s/The-1791-Excise-Whiskey-Tax/, accessed September 28, 2021.

We can help with your tax matters involving a full-range of state and local tax issues. Contact Tax Division leader Jackie Cook jjc@novaralaw.com. Tax lawyer Kimberly Cloud contributed to this article.